[ad_1]

We’re in a double bind proper now. Costs are going by the roof however all of the indicators counsel that the economic system is weakening. The reply to larger costs is often to lift rates of interest, however this additionally induces folks and companies to spend much less cash. The problem for central banks is to try to take care of each issues on the identical time.

We requested three economists whether or not they noticed a approach of bringing down inflation with out inflicting a extreme recession. Right here’s what they mentioned:

Jonathan Perraton, Senior Lecturer in Economics, College of Sheffield

The Financial institution of England’s determination to lift rates of interest by a comparatively modest 0.25 share factors to 1.25% contrasts with the US Federal Reserve’s 0.75 factors hike the day earlier than to a spread of 1.5% to 1.75%. This displays issues within the UK that financial development can be weaker than beforehand forecast.

It follows the sudden information that the UK economic system shrank by 0.3% in April, plus sobering forecasts from the Organisation for Financial Co-operation and Improvement (OECD) that the UK would be the worst performing main economic system in 2023 aside from Russia. GDP is now solely fractionally above its pre-COVID degree and all main sectors are shrinking.

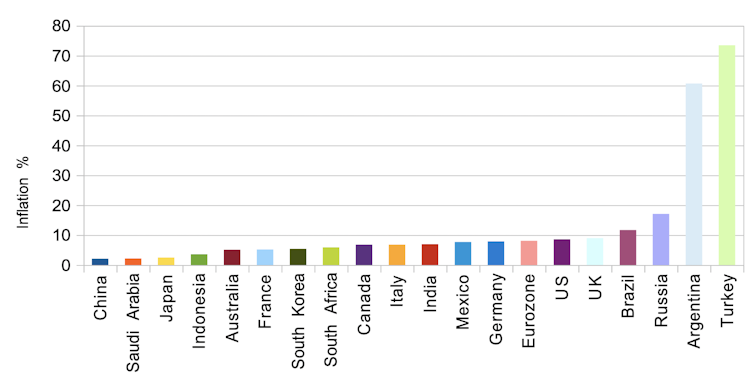

The Financial institution of England’s warning is regardless of inflation at present being at 9% and now anticipated to succeed in 11% within the coming months. These are ranges not seen because the Nineteen Eighties. Forecasts have the UK experiencing one of many highest inflation charges of the main economies.

Inflation charges within the G20

Varied sources

Inflation is a worldwide drawback because of pressures on provide chains after COVID and better vitality and different commodity costs following Russia’s invasion of Ukraine. Nonetheless, US economist Adam Posen has pointed to Brexit as a key consider explaining Britain’s comparatively excessive inflation. This has meant larger buying and selling prices, weak sterling and labour shortages.

Unemployment has fallen to solely 3.8%, though employment charges are nonetheless under pre-COVID ranges, pointing to extra folks being inactive – notably older employees. Employees shortages have turn into a key function of the British economic system.

You would possibly count on this mixture of low unemployment and unfilled vacancies to drive up wages. As a substitute common pay, excluding bonuses, fell by 2.2% in actual phrases in June, the biggest fall for over 20 years. So at the very least this doesn’t but seem like a traditional wage-price inflationary spiral, the place companies give solution to calls for from employees for larger pay, move on the prices to shoppers within the type of larger costs, and employees demand even larger wages to manage. Having mentioned that, bargaining rounds are but to be accomplished and we’re seeing extra wage disputes in some sectors.

Till now, shopper demand has helped to stimulate financial exercise within the UK, however this has partly been sustained by family financial savings. A few of this displays households now spending extra as COVID restrictions have been lifted however there are clear limits to how far households can dip into their financial savings as dwelling requirements are squeezed. Not surprisingly, shopper confidence is falling.

Paul Melling/Alamy

Long term issues additionally stay. UK productiveness has been very weak because the 2008 world monetary disaster. There are lots of doable explanations, together with weaknesses in capital funding and coaching – the latter mirrored in present difficulties in filling vacancies.

In sum, the Financial institution of England is going through unprecedented challenges. Rate of interest rises are a blunt instrument to take care of supply-side issues in a British economic system the place development is grinding to a halt. So long as inflation outstrips wages and the economic system stagnates, it’s prone to fall on the federal government reasonably than the Financial institution of England to offer folks with assist.

Brigitte Granville, Professor of Worldwide Economics and Financial Coverage, Queen Mary College of London

Stagflation is upon us, so a pure focus for any “the place subsequent?” dialogue have to be whether or not we’re on target for an episode as unhealthy because the Seventies and even worse. My reply can be that recession is probably going, however the Seventies expertise of excessive inflation persisting regardless of repeated recessions needs to be avoidable. That mentioned, even a comparatively milder dose of stagflation can be painful for dwelling requirements.

The mildest approach out of the current scenario can be inflation promptly curing itself: by making folks poorer in actual phrases to allow them to’t afford to purchase a lot. On this state of affairs, inflation would ease and central banks might assist with the downturn within the economic system by reversing their current interest-rate hikes.

There are a number of obstacles to such a quick turnaround, nevertheless: the context of the post-COVID restoration and the labour market.

The principle inflationary impulse has come from two elements on the worldwide provide aspect. First, provide chains have struggled to deal with demand collapsing and resurging throughout and after COVID, made worse by China’s zero-COVID coverage. Second, vitality and different pure useful resource provides have been constrained by Russia’s conflict in Ukraine and the west’s sanctions.

The inflationary results of those points are being extended by pent-up demand from western companies and shoppers because of COVID stimulus packages within the UK and particularly the US, in addition to unspent revenue accrued throughout lockdowns. Within the UK, for instance, family deposit balances had been nonetheless properly above pre-COVID ranges as lately as April.

It doesn’t assist that the monetary markets have been pushed to such heights by unfastened financial coverage. Though the bubbles have been popping lately, valuations should fall a way additional earlier than folks really feel poorer and fewer keen to exit and purchase issues.

Poring Studio

Turning to the second impediment to a fast reversal of the inflation surge, particularly the labour market, the primary drawback once more comes from the availability aspect. Labour demand from companies has normalised post-COVID, however there are too few employees. That is partly to do with extra folks over 50 selecting not to return to work, however the UK has the extra drawback of Brexit interrupting the circulate of excellent high quality labour from central and jap Europe.

With too few employees, corporations are being pressured to pay folks extra – UK wages are rising at about 4% a 12 months – and to move on the associated fee to prospects within the costs of products and providers. Alert to the specter of a Seventies-style wage-price spiral, the Financial institution of England has been elevating rates of interest.

However main indicators counsel that the wage-price spiral menace shouldn’t be that critical. The carefully watched Buying Managers’ Index, which gauges UK corporations’ optimism concerning the economic system, reveals that these in providers have gotten gloomier concerning the coming months. You don’t hold growing costs in case you suppose persons are going to cease shopping for. And whereas we might have seen faint echoes of Seventies-style labour militancy in transport, as an illustration, pessimistic corporations are typically extra prone to lower hiring plans and output reasonably than give solution to hefty wage calls for – if not shut up store altogether.

It appears to me that this can be extra decisive in figuring out the course of inflation since it’s a long-term structural concern, whereas the post-COVID points ought to ultimately straighten out. So total, I count on that the UK economic system’s current stagnation, fairly possible dipping into gentle recession, will deliver inflation again down in the direction of the two% goal. Within the US, the place underlying demand and credit score is stronger, sharper curiosity hikes could also be wanted to realize the identical purpose.

The principle hazard for my part is central banks changing into too dogmatic about their 2% inflation targets. In my e-book Remembering Inflation, I reviewed convincing analysis findings that inflation ranges as much as 5% trigger little or no long-term injury to development – particularly if the inflation charge is regular reasonably than risky. So as soon as inflation eases slightly, central banks ought to cease mountaineering rates of interest to keep away from doing extra hurt than good.

Chris Martin, Professor of Economics, College of Tub

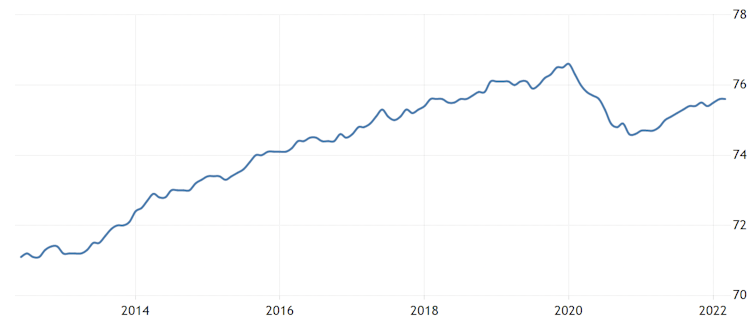

The UK labour market goes to be key to how the UK economic system performs within the coming months, and its prospects are finely balanced. On one hand, it proved resilient in the course of the pandemic. The furlough schemes had been successful, defending the labour market from the worst results of the disaster. The autumn in employment was round 3 times decrease than within the Seventies, though the financial contraction was a lot higher.

Employment additionally recovered extra shortly than in earlier recessions. Vacancies are over 50% larger than earlier than the pandemic. Common wages excluding bonuses are rising by about 4% a 12 months, with even larger development for drivers and employees in building, software program growth and warehousing.

UK employment charge (%)

Buying and selling Economics/ONS

Then again, employment continues to be decrease than earlier than the pandemic by near 250,000 employees. Actual wages are still no higher than in 2008. And the macroeconomic context is gloomy: it’s arduous to see how the labour market will thrive if development is weak or non-existent.

A number of elements make the following few months arduous to evaluate. First, unemployment is now not a helpful labour market indicator. Staff are these days categorised as employed, unemployed or inactive. Unemployed employees are actively in search of work however the inactive will not be. Of the circa 250,000 drop in employed employees since 2019, 80% are inactive; solely 20% are actually unemployed.

Economists have a a lot weaker understanding of the inactive than the unemployed. This issues as a result of most individuals getting employed are from the inactive reasonably than the unemployed class.

Second, maybe surprisingly, Brexit has not decreased migration, but it surely has changed it. There are fewer EU residents employed within the UK, however extra employees from Nigeria, India and related international locations. They are typically extra extremely expert and to work in well being and social care, reasonably than in hospitality.

Extra expert employees needs to be good for productiveness and fill important roles in well being and social care, however hospitality is struggling on the identical time. Nonetheless, it isn’t but clear if these adjustments are everlasting, and this too makes the labour market tougher to forecast.

As well as, the behaviour of vacancies and their relationship to hiring appears to have modified. The newest knowledge reveals 1.3 million vacancies, round 40% larger than pre-pandemic. However this has not resulted in document numbers of employees being employed. Regardless of the trigger, we will now not depend on excessive emptiness posting to generate rising employment.

Lastly, a putting divide is opening between the private and non-private sectors. Personal sector employment is again to pre-COVID ranges, however public sector employment lags behind. Personal sector wages are at present growing by 8%, in comparison with simply 1.5% for the general public sector. Forecasting public sector employment is troublesome, since it’s proof against a few of the market forces that drive the non-public sector, though there appears little prospect of noticeable development over the following few months.

So what’s the outlook for UK employment? Above all, companies are prone to be searching for fewer employees as power weak funding and slowing shopper expenditure factors to stagnant or falling GDP.

These detrimental forces can be offset by the massive variety of vacancies at present being supplied by companies and by comparatively giant wage rises in some elements of the non-public sector. This may occasionally induce a few of these employees again into the labour market who’ve withdrawn following the pandemic.

On stability, I might count on a fall in employment of as much as 100,000 employees within the coming few months. That’s lower than 0.1%, so it’s not going to enormously exacerbate all the opposite issues within the economic system.

[ad_2]

Source link

{kind=link}